Is Investing Too Complicated?

Investor Deprogramming Series: Part III

Welcome to issue #18 of The Davem Dish. Every two weeks I share what actually works in investing based on my 20 years of wins, losses and expensive lessons. You’ll also get my thoughts on solopreneurship and life in general because the same principles apply — keep it simple, stay consistent and focus on what matters.

Part III of my Investor Deprogramming Series explores the question of whether investing is too complicated for regular people. In this five part series I’ll dive into “common wisdom” that may be sabotaging your wealth.

You want to learn to invest. Not passive investing — you already know to put money in low-cost index funds and let compound interest do its magic.

I mean really invest. How to pick individual companies and build wealth on your terms.

So, you do what any serious person would do. You start reading. That’s what I did.

The Intelligent Investor, One up on Wall Street, How to Make Money in Stocks, Common Stocks and Uncommon Profits. Anything said or written by Warren Buffett.

All good sources written for average investors by investing legends. And the messages are surprisingly simple and empowering:

Think like a business owner, not a trader

Invest in what you know

Buy good companies at reasonable prices and hold long term

You don’t need to be a genius, just patient and disciplined

You finish the books feeling optimistic. This doesn’t seem that hard.

Following the Instructions

Next you do what the legends say.

Warren Buffett famously read annual reports and other SEC filings 5-6 hours each day. He’s said to have made his Coca-Cola investment decision entirely from reading the annual report.

So, you pull up your first annual report for a company you’re interested in.

Then an earnings call transcript.

Within a minute, you encounter something like this:

“We saw sequential margin expansion driven by favorable mix shift and operating leverage, though headwinds from FX and a normalization of channel inventory created some pressure on our run-rate. Our adjusted EBITDA came in at the high end of guidance, and we remain constructive on the forward outlook given secular tailwinds in our TAM...”

What does this even mean?

But the CEO sounds very confident. The analysts asking questions seem to understand. They’re using terms like “accretive to EPS,” “capital allocation framework,” and “normalized free cash flow yield.”

You Google some of these terms and every definition contains three more terms you don’t know.

The jargon soup includes:

Valuation speak: Multiple expansion/compression, EV/EBITDA, forward vs. trailing P/E, DCF, NAV, intrinsic value

Growth speak: Organic vs. inorganic growth, comps, run rate, YoY, QoQ, sequential growth, CAGR, accretive/dilutive

Earnings call buzzwords: “Provide some color,” guidance, beat/miss, consensus estimates, whisper number, adjusted earnings, non-GAAP, “normalized” earnings, one-time items

Market lingo: Risk-on/risk-off, flight to quality, rotation, beta, alpha, drawdown, mean reversion

Analyst ratings: Overweight, underweight, outperform, neutral, “constructive”

I could go on but I think you get the point.

Instead of gaining more clarity, you’re more confused than before you started.

Am I not smart enough for this?

Everyone else seems to understand. The analysts, the fund managers, the CNBC commentators all nodding along.

Maybe investing really is for smarter people. I’m probably better off handing my money over to the professionals.

But… you were SUPPOSED to feel lost. That’s the point.

The confusion isn’t a sign you’re not smart enough. It’s a sign the system is working exactly as designed.

Trained to Sound Unscripted

It took me a few years to understand that following the instructions perfectly leads you astray.

The books said to read annual reports so you did, but you got more confused, not less.

This isn’t a failure of effort or lack of intelligence, it’s a context mismatch.

Warren Buffett read annual reports when that was the ONLY information source. There was no CNBC and no internet. If you wanted to understand a company, your only option was to read what the company published.

The legends’ principles are timeless but their tactics were era-specific.

Don’t confuse the two.

When I started investing, I followed the instructions and I’d print annual reports and studied in my free time.

I read a lot of reports and took notes, but I didn’t feel like I was learning all that much. It was a lot of verbiage that didn’t really tell me anything.

Then I started working with my company’s Investor Relations department.

That’s when I discovered every word and graphic in those SEC filings and earnings calls is highly scripted. Executives have coaches and media training. They spend weeks preparing a story, rehearsing answers, strategizing about what questions analysts will ask.

Executive coaches help CEOs “speak conversationally and with genuine enthusiasm that helps the remarks feel unscripted.”

Read that again. Executives are trained to make scripted remarks feel unscripted.

And what really matters is the audience isn’t you.

Their job isn’t to inform regular investors — it’s to attract institutional investors while making you feel included.

Why do you think only professional analysts get to ask questions on earnings calls?

Why do companies attend invite-only meetings with banks and top shareholders — meetings you’ll never be invited to?

Jargon Exists for a Reason

The complexity serves two purposes:

First, efficiency among professionals who use these terms daily. Ok, fair enough.

Second, creating a barrier that makes outsiders feel like they need an expert to translate.

This is by design.

The financial services industry wants you to believe investing is too complicated for regular people. “You need us. Trust us and pay our fees”

The jargon, the scripted presentations, the analyst reports that are somehow longer and more complex than the documents they’re summarizing — all of it reinforces the same message. You can’t do this yourself.

Even pop culture reinforces the myth. Take the popular movie, The Big Short. While explaining the 2008 financial crisis and translating complicated financial instruments into layperson terms, it also sent a clear message — understanding finance requires genius-level intelligence. The protagonists were portrayed as brilliant outliers who could see what others couldn’t. Reinforcing the myth that regular investors can’t compete.

What the movie didn’t tell you was those complex instruments (CDOs, synthetic CDOs, credit default swaps) are NOT what regular investors need to understand. They are Wall Street products designed for institutional speculation, not individual wealth building.

You don’t need to understand synthetic CDOs to beat the market. You need to understand whether a company makes money and is priced reasonably.

The CNBC Trap

So next you turn on financial news for “education.”

What you get instead:

One manager says BUY, another says SELL — on the same stock, same day

Talking heads confidently predicting the market will go up, followed immediately by someone confidently predicting it will crash

Price targets on the same stock ranging from $400 to $600

Urgent “breaking news” that moves markets before you can react

I’ll never forget watching CNBC during the dot-com bubble. The building electricians at my summer job loved watching their portfolios grow. “Look at these charts — this is easy money. I’m going to retire early!”

Then the bubble burst. Everyone who was a genius went back to their day jobs with a much smaller portfolio and a feeling of “what could have been.”

I just wanted answers to basic questions: How do you know what a company is worth? When should you buy and when should you sell?

The “answers” depended on which CNBC expert you believed that day. But those aren’t real answers — just promoted opinions.

The financial media business model isn’t to make you a better investor. It’s to keep you watching. Conflict, urgency, and complexity drive engagement.

Confidence and boldness sells, even when it’s baseless.

What Now?

At this point, most people reach one of two conclusions:

The game is rigged. I can’t compete so I’ll just buy index funds and forget about it — or worse, I’ll do nothing.

This is too complicated. I’ll hire a professional.

Both conclusions benefit the financial services industry. You hand over your money — and pay fees that cost you 17% of your final wealth over 20 years (as I covered in Part II of this series).

But here’s what the data actually shows:

65% of large-cap fund managers underperformed the S&P 500 in 2024

Over 15 years, not a single category saw a majority of active managers beat their benchmarks

The average hedge fund returned 6.9% annually from 2009-2019 versus 13.6% for the S&P 500

The smartest people on Wall Street — delivered half the returns of doing nothing except buying an index fund.

So, if the professionals can’t beat the market with all their complexity...

Maybe complexity isn’t the advantage?

The Conflation Problem

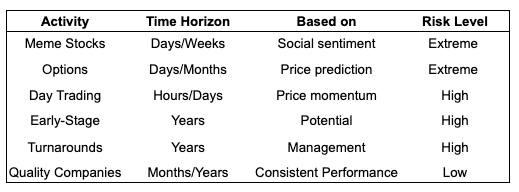

There’s another common pitfall for new investors. People tend to lump different kinds of investing and different kinds of companies together.

Watching CNBC, scrolling social media, talking to neighbors — you’ll hear about:

Meme stocks

Options plays

Day trading

Early-stage companies

Turnarounds

Quality compounders

These are different investment strategies and different kinds of companies. They are treated as variations of the same activity but they’re not.

Specific to companies, here’s an analogy. Say you graduate from a top business school. You’re a “hot prospect” but you have debt and no job yet. You’re an early-stage company. There’s a chance — maybe even a good chance — you do well. But right now, you’re speculative. Investing in you is a bet on potential, not consistent performance.

Whereas if you’ve been moving up the corporate ladder for 20 years and now are a senior executive — you’re a quality company. A consistent track record of performance and a consistent earner. You may pivot and change careers but you’re a “known commodity”. Investing in you presents less risk.

These distinctions matter because the strategies are completely different.

Notice something?

Investing in quality companies is the ONLY low-risk option.

Most of what people call “investing” is actually speculation.

The entire financial media ecosystem is built around high-risk activities because they’re more dramatic and more engaging. Nobody makes viral TikToks about patiently holding quality compounders.

But that’s exactly what builds wealth over the long-term.

What Actually Matters

Strip away the jargon, the scripted presentations, the noise and what’s left?

Something simple.

Stock prices for mature, quality companies reflect current earnings and future expected earnings.

Which means the most important thing to track is… earnings growth.

But earnings can’t consistently grow without sales growth.

When sales are generated, quality companies do what you should with your personal finances — control spending to retain as much cash as possible.

The cash retained needs to be invested to create value.

That’s where metrics like Return on Equity (ROE) and Return on Invested Capital (ROIC) come in.

Make money → Keep money → Invest money → Make more money

That’s basically it. That’s the entire framework.

You don’t need to decode “sequential margin expansion driven by favorable mix shift.”

You need to know are earnings growing? Are sales growing? Is the company making smart investments with its cash?

This information is freely available and no jargon translation is required.

A company’s historical track record also tells you whether management delivers. Not puff pieces about visionary CEOs, not scripted earnings calls, not analyst reports with made-up price targets.

You just need to follow the numbers. Did they grow or didn’t they?

And the math isn’t hard. It’s percentages.

The Real Edge

Your edge as an investor isn’t analytical. It’s structural and behavioral.

Structural advantages over professionals:

No SEC rules forcing diversification

No career risk for taking contrarian positions

No redemption pressure forcing you to sell at the wrong time

No quarterly performance reporting

No committees or bureaucracy

Behavioral edge (if you develop it):

Ability to be patient when others panic

Willingness to buy when prices drop

Discipline to cut losses short

Systems that remove ego, emotion, and bias

The classic books were right all along. Investing isn’t too complicated.

What’s complicated is the theatre built around it — the jargon, the scripted performances, the conflicting predictions, the conflation of investing with speculation.

That complexity exists to benefit the financial industry, not you.

Strip away the performance and you’re left with what all the legends taught:

Understand what you own

Buy quality companies at reasonable prices

Think in years, not days

Have a process

Ignore the noise

It’s not that individuals CAN’T beat the market — it’s that most WON’T.

With the right framework and mindset, you can be the exception.

Cheers,

Andrew

Do you have what it takes to beat the market? Take my free 3-minute assessment to find out what might be holding you back.

Coming up in Part IV: Does “Buy and Hold” actually work?

Thanks for reading The Davem Dish! If you enjoyed this issue, feel free to subscribe and share it with other awesome people like you.

The content provided are personal opinions and presented for educational purposes only, as of the date published or indicated. Davem Advisors LLC is not a bank, licensed securities dealer, broker or investment advisor. Displayed returns are unaudited. Nothing stated constitutes a recommendation or advice as to whether any investment is suitable for a particular investor. You alone are solely responsible for determining whether any investment, strategy or service is appropriate for your objectives. Past performance is no guarantee of future results. Inherent in any investment is the risk of loss.