Does Buy and Hold Actually Work?

Investor Deprogramming Series: Part IV

Welcome to issue #19 of The Davem Dish. Every two weeks I share what actually works in investing based on my 20 years of wins, losses and expensive lessons. You’ll also get my thoughts on solopreneurship and life in general because the same principles apply — keep it simple, stay consistent and focus on what matters.

Part IV of my Investor Deprogramming Series explores the question of whether Buy and Hold actually works. In this five part series I’ll dive into “common wisdom” that may be sabotaging your wealth.

“My favorite holding period is forever.”

Another Warren Buffett classic. One of the most repeated investing quotes of all time. Ask any kid what they know about investing and they’ll probably say something about Buy and Hold.

The advice sounds so simple.

Find a good company. Buy shares and check back years later when you’re rich.

And to reinforce that narrative we see examples like this all the time.

If you bought NVIDIA in 2015 and held through today, you’d be looking at returns of over 23,000%. Generational wealth from a single position.

But is it that simple? Does Buy and Hold actually work?

The Gospel of Buy and Hold

Let’s start with where this advice came from.

In 1973, Princeton economist Burton Malkiel published A Random Walk Down Wall Street. His central argument was that if markets are efficient, trying to beat them is futile. Just buy everything and hold it.

A few years later, John Bogle launched the first index mutual fund at Vanguard. The initial offering wasn’t a success — he only raised about 5% of what he hoped for — but eventually the indexing strategy eventually caught fire. Today it’s widely endorsed as the central tenet to investing success.

But neither Malkiel nor Bogle advocated Buy and Hold for individual companies. In fact, they warned against it. Somewhere along the way, the message got twisted. “You can’t beat the market, so buy the whole market” became “buy good companies and hold them forever.

The Misinterpreted Quote

Let’s go back to Buffett’s famous line. Here’s what he actually said:

“When we own portions of outstanding businesses with outstanding managements, our favorite holding period is forever.”

The qualifier “outstanding businesses with outstanding management” is not “Buy and Hold forever”, it’s “buy exceptional companies and hold them as long as they remain exceptional.”

This is very subjective. What exactly is the criteria for “exceptional”? Buffett and Berkshire decide what works for them. That might not be what works for you.

In 2024 alone, Berkshire exited several positions in companies such as Floor & Decor, T-Mobile, and Ulta Beauty.

Ulta Beauty was a position added in 2024, only to be sold within the same year. Not exactly holding forever.

Buffett sells stocks all the time. In the three years leading up to his retirement in 2025, he was a net seller of stocks in every single quarter.

But the soundbite lives on without the context.

You’ve been told to do something the originators warned against, by someone who doesn’t do it himself.

The Historical Data

In 2017, finance professor Hendrik Bessembinder published research where he examined every U.S. stock traded on the major platforms since 1926.

The findings:

57% of individual stocks underperformed Treasury bills over their entire lifetime.

Most stocks — not some, MOST failed to beat cash over the long run.

It gets worse.

Only 4% of stocks accounted for ALL of the stock market’s wealth creation since 1926.

The other 96% of stocks? They collectively matched Treasury bills.

When Bessembinder ran simulations of randomly selecting one stock each month from 1926 to 2016:

96% of these strategies underperformed the market

73% underperformed Treasury bills

If you’re picking individual stocks randomly and holding them forever, you’re playing a game where the odds are stacked against you 96% to 4%.

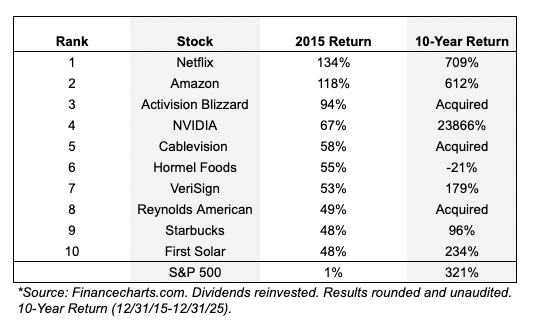

A Case Study

In 2015, NVIDIA was the #4 best-performing stock in the S&P 500, up +67%. It was a solid GPU company serving gamers and data centers.

Nobody knew it would become the backbone of the AI revolution.

But that’s survivorship bias talking. NVIDIA is one of the 4%. For every NVIDIA, there were 24 other stocks that didn’t work out.

Let’s make this concrete.

The S&P 500 returned just 1.4% in 2015 — basically flat. But some stocks did well.

Here were the top 10 performers:

Imagine you bought all ten winners in 2015 and committed to holding forever.

Ten years later, here’s what actually happened:

Cablevision — Acquired by Altice in 2016. Forced out.

Reynolds American — Acquired by British American Tobacco in 2017. Forced out again.

Activision Blizzard — Acquired by Microsoft in 2023. Cashed out whether you wanted to or not.

Hormel Foods — Lost 21% over 10 years.

Starbucks — Good run, then collapsed. Currently down ~35% from 2021 high.

First Solar — Crashed after 2015. Highly volatile.

Out of 10 winners in 2015 only three were genuine Buy and Hold success stories: Amazon, Netflix and NVIDIA.

That’s a 30% success rate on a list that was ALREADY cherry-picked to include only the top performers.

Stated another way — even if you started with winners, you failed 70% of the time before psychology entered the picture.

And that assumes you could have identified those three in advance. The obvious problem is knowing which ones are the winners before they win.

Also, would you have had the discipline to hold the whole time? Psychology says no.

That 23,000% gain if you bought NVIDIA ten years ago. Would you have sold it after it was up 100%, or when dropped over 50% in 2022 before skyrocketing again in 2023?

What about when Netflix and Amazon were both down 50% in 2022?

Skewed Data

When people show you historical returns proving Buy and Hold works, they’re using data contaminated by survivorship bias.

Survivorship bias means the failures — the bankruptcies, the delistings, the acquisitions at pennies on the dollar — vanish from the dataset.

How bad is the distortion?

A 10-year historical dataset for North American stocks is missing approximately 75% of the stocks that were actually trading during that period.

Three out of four stocks just disappear from the analysis.

One study tested a momentum strategy on the Nasdaq 100:

With survivorship bias: 46% annual returns, 41% max drawdown

Without survivorship bias: 16.4% annual returns, 83% max drawdown

Same strategy and same time period. Different reality.

When someone says “if you had just bought [famous stock] back then...” they’re engaging in survivorship bias. They’re not showing you the 96% of stocks that didn’t work out.

The past looks rosier than it was because the losers have been erased.

The Collapse of Actually Holding

The irony is everyone says Buy and Hold and almost nobody does it.

The average stock holding period:

1950s: 8 years

1987: Under 2 years

2007: ~7 months

2020: 5.5 months

Despite decades of Buy and Hold advice, actual holding periods have collapsed by 95%.

Why?

Because human psychology — combined with easy access to trading platforms with zero online commissions — makes true long-term holding nearly impossible.

Terrance Odean, a finance professor at UC Berkeley, analyzed 10,000 brokerage accounts and discovered something interesting:

Investors are 60% more likely to sell their winning stocks than their losing stocks.

When a stock goes up, we want to “lock in the profit.” When a stock goes down, we hold on hoping it recovers.

This is the disposition effect, and it costs investors about 4.4% annually in lost returns.

We systematically sell our best performers and keep our worst ones.

The four psychological forces driving this behavior:

Loss aversion — The pain of a loss is felt twice as intensely as the pleasure of an equivalent gain. We become risk-averse when stocks are up (wanting to “lock in gains”) and risk-seeking when down (hoping for recovery).

Mental accounting — We mentally track each position against its purchase price. Selling a loser means converting a “paper loss” into a “real loss” — admitting we were wrong.

Regret aversion — Selling a stock that later rises creates intense regret. Holding a loser lets us pretend the loss is “only temporary.”

Self-control failures — Even investors who recognize these biases can’t overcome them. As one researcher stated “Individual investors do not lack prediction skills. They lack discipline.”

So even if Buy and Hold were the optimal strategy, most investors are psychologically incapable of executing it.

The advice says “hold your winners.” The psychology says “sell your winners.” These aren’t compatible — unless you build selling into the process from the start.

The Cisco Test

Let me show you how this plays out with a real example.

A high-flyer of the dot-com era was Cisco Systems. In March 2000, Cisco became the world’s most valuable company. Their routers and hardware were building the backbone of this new thing called the Internet. The stock hit an all-time high of $80.

John Chambers was a well-respected CEO who held the top job for 20 years, practically forever in CEO terms. From 2000 to 2015, the company more than doubled sales from $19 billion to $49 billion.

Good company. Good management. Checked all the boxes.

How did Buy and Hold work out?

If you bought near the peak in July 2000 at $65 and held until Chambers stepped down in July 2015, you watched the stock price shrink to $27.

Total return: -58.5% Average annual return: -5.7%

You might argue this is skewed by the dot-com crash. Fine. Let’s look at 2005 to 2015.

During this decade, Cisco mostly traded in a range from $15 to $30. That’s 100% total return, about 7% annually.

Better than losing money. But still lagging the S&P 500 historical average.

Buy and Hold with Cisco — a quality company with quality management — gave you mediocre results at best and severe losses at worst.

Just this past May Cisco finally eclipsed its dot-com peak — 25 years later.

So if “hold forever” doesn’t work, what does? Let me show you a different approach with Cisco during the same decade.

A Different Approach

Instead of Buy and Hold, what if you used a systematic process?

Identifying misalignment between price and value, following pricing patterns and selling with trailing stops to lock in profits.

If our analysis indicated that Cisco continued to meet quality criteria and was undervalued, we would look at support levels as investment opportunities.

How would that have played out?

Investment #1:

2/9/2009: Buy $14.50 (support level)

5/24/2010: Sell $22.60 (trailing stop triggered)

56% gain in 15 months

Investment #2:

8/15/2011: Buy $14.50 (support level)

4/30/2012: Sell $17.20 (trailing stop triggered)

19% gain in 8 months

Investment #3:

7/16/2012: Buy $15.00 (support level)

10/28/2013: Sell $21.30 (trailing stop triggered)

42% gain in 15 months

All short-term. All significantly better than the 7% annual Buy and Hold return during the same period.

Does this approach take time and effort? Yes, but probably less than the time you spend daily scrolling social media.

Is it difficult? Not really. You mostly just need to be consistent and follow patterns.

Can you do this yourself and earn above-market returns? Absolutely.

The Real Lesson

Buy and Hold works for index funds. You’re buying the entire market, which mathematically captures the 4% of stocks that drive all returns. You’re dollar cost averaging and reinvesting dividends. You don’t need to pick winners because you own all of them.

But that’s not what this newsletter is about. If you want average returns, buy an index fund and go enjoy other activities.

We believe we can beat the market. The question is how.

It isn’t “holding forever”. It’s having a process.

For individual stock investors, Buy and Hold is advice most people have rarely done themselves successfully, using data that systematically excludes all the failures, for a time period the investor will almost certainly not maintain.

The question isn’t whether Buy and Hold can work.

The questions are:

Which stocks to Buy and Hold

When holding becomes a mistake

How to overcome the psychology that makes true long-term holding nearly impossible

Buy and Hold assumes you can identify the 4% — but gives you no process to do it.

A systematic approach flips the script. Find quality companies, wait for price to misalign with value, and use systematic exits to lock in gains. Not hold forever. Hold until the price tells you otherwise.

Buy and Hold isn’t a strategy for investing in individual companies. It’s the absence of one.

Cheers,

Andrew

Think you can find the 4%? Or would you rather have a process that doesn’t require you to? Take my free 3-minute assessment to find out what might be holding you back.

Coming up in Part V: Is the stock market rigged?

Thanks for reading The Davem Dish! If you enjoyed this issue, feel free to subscribe and share it with other awesome people like you.

The content provided are personal opinions and presented for educational purposes only, as of the date published or indicated. Davem Advisors LLC is not a bank, licensed securities dealer, broker or investment advisor. Displayed returns are unaudited. Nothing stated constitutes a recommendation or advice as to whether any investment is suitable for a particular investor. You alone are solely responsible for determining whether any investment, strategy or service is appropriate for your objectives. Past performance is no guarantee of future results. Inherent in any investment is the risk of loss.