Do You Need a Financial Advisor?

Investor Deprogramming Series: Part II

Welcome to issue #17 of The Davem Dish. Every two weeks I share what actually works in investing based on my 20 years of wins, losses and expensive lessons. You’ll also get my thoughts on solopreneurship and life in general because the same principles apply — keep it simple, stay consistent and focus on what matters.

Part II of my Investor Deprogramming Series explores whether you need a financial advisor. In this five part series I’ll dive into “common wisdom” that may be sabotaging your wealth.

Happy New Year!

I was talking to a family member over the holidays who was praising their new financial advisor.

“Ron has made us a lot of money.”

Oh really? What are you invested in?

“I don’t know — here’s a statement, but there’s a lot of information here and I don’t really know what I’m looking at.”

This is by design, I thought but said nothing.

The stock holdings looked like a basket of S&P 500 companies. I asked what’s the strategy?

“Holding winners and selling underperformers. They’ve been doing this a long time and it always works.”

What does “always works” mean? Do you have evidence?

“I don’t know.”

I continued, is your performance better than just holding a S&P 500 index fund? Is Ron actually making you money or are you making money because the market has been up?

“I don’t know.”

Have you calculated how much you’ve paid Ron and your previous advisor over the years?

“No, but I think it’s been a lot.”

I could sense she was getting irritated with my questions, so I changed the subject.

What struck me later was this person is a semi-retired accountant and business owner. She looks at her portfolio regularly and has more financial literacy than most people. In fact, on multiple previous occasions she lamented how much she was paying in fees and how her previous advisor missed opportunities by selling Apple and Amazon too early. And yet she’s been programmed to believe she can’t manage her own money.

“It’s a lot of work and I don’t want to mess with it.”

That final comment says it all. It’s not that people are lazy or unintelligent. It’s learned helplessness and an entire industry profits from it.

This isn’t a post bashing financial advisors. Some advisors provide general value — tax planning, estate coordination, and coaching in addition to portfolio management.

If you have a complex financial situation, trust your advisor, and feel the work justifies the fees, this post isn’t telling you to fire anyone.

But here’s the question you should be able to answer: Is your advisor actually making you money, or is the market making you money while your advisor takes credit?

Most people can’t tell the difference.

The 1% Fee That Costs You 17%

The Assets Under Management (AUM) dominates the industry with more than 85% of advisors using it as their primary pricing model. AUM fees vary depending on the size of your portfolio, but for simplicity we’ll use 1%.

This may not seem like much but let’s run the math on a $500,000 portfolio over 20 years assuming 8% annual returns.

Without the 1% fee: $2,330,479

With the 1% fee: $1,934,842

The difference: $395,637

Your advisor will collect roughly $186,000 in fees over those 20 years. You didn’t just lose $186,000 though. You lost $395,637 — because every dollar paid in fees is a dollar that can’t compound. The magic of compounding working against you.

That 1% annual fee costs you 17% of your final wealth.

The industry hopes you never do this math.

The 3% Myth

The industry claims advisors add roughly 3% annually through behavioral coaching, tax optimization, and rebalancing. If true, a 1% AUM fee may be justified.

But here’s the issue:

The 3% “alpha” is theoretical and highly variable by individual. It assumes you would make catastrophic behavioral mistakes without guidance — panic-selling in crashes, chasing performance, trying to time the market. Disciplined investors who follow a simple plan don’t make $400,000 worth of behavioral mistakes.

Tax-loss harvesting doesn’t apply to tax advantage retirement accounts. Tax-loss harvesting — selling losers to offset gains — is marketed as a value-add service. But it provides zero benefit in IRAs, 401(k)s, and other tax-advantaged accounts where most Americans hold their retirement savings.

The Robo-Advisor Mirage

Perhaps you’re skeptical of traditional financial advisors but still want some guidance. Robo-advisors may be an option. These are automated investment platforms that build and manage portfolios for around 0.25% annually compared to 1% for a traditional human advisor.

Strip away the marketing and ask what your actually paying for:

Portfolio construction based on a risk questionnaire.

Automatic rebalancing when allocations drift.

Tax-loss harvesting (which, again, doesn’t apply to retirement accounts).

For a $500,000 porfolio, you’re paying $1,250 per year for automatic rebalancing and a preset ETF allocation.

A Vanguard Target Retirement Fund does essentially the same thing for 0.08% — that’s $400 per year.

Over 20 years, even the “low-cost” robo-advisor fee costs you $114,180 in lost wealth.

Is that worth it for a service you could replicate with a single fund and 15 minutes of annual attention?

The Neighborhood Advisor

Let’s move on from licensed financial advisors to what I’ll call “neighborhood advisors”. A bit surprisingly, a 2025 Gallup survey found almost 45% of Americans still turn to friends and family for financial guidance and 20% turn to social media.

At first glance, this is alarming. You might think the last people you should take advice from is your Uncle Frank or some finfluencer’s hot takes on social media.

However, in an era of unprecedented (and mostly free) access to information, education tools, and real-time market data, I believe there are neighborhood advisors who are worth listening to. People in your life or on social media who have built real wealth through disciplined investing.

But, with key qualifiers:

A long track record of actual performance. Not just opinions and what-ifs.

A documented, repeatable process you can understand and verify.

Transparency about both wins and losses.

A friend who’s beaten the S&P 500 for a decade with a simple, explainable strategy may be more valuable than a credentialed advisor who can’t answer basic questions about your portfolio.

Hunches aren’t a process, but neither are credentials without results.

The Real Question

Whether you hire a financial advisor, use a robo-advisor, listen to a neighborhood advisor, or manage your own money, one thing is clear:

You must develop financial literacy.

Understanding how compounding works. What actually moves markets and stocks. What information actually matters and how to value a company. When to buy and when to sell. How to limit emotion and biases.

This isn’t optional knowledge you can outsource forever. Because even if you hire someone else to manage your money, you’re still responsible for managing them and making sure you’re receiving the value you’re paying for.

My relative couldn’t answer a single question about her own portfolio. She didn’t know the strategy, her performance relative to benchmarks, or her total fees paid. She outsourced not just the work but the thinking. It worked in recent years, but will it work forever?

You don’t have to manage your own investments but you do need to understand them.

And you don’t have to become a market expert. But you should know enough to recognize when you’re paying 17% for peace of mind you could build yourself.

Isn’t your financial future important enough to find out?

2025 Davem Watchlist Recap

In Parts I and II of this Investor Deprogramming Series I’ve questioned whether professional money managers can beat the market.

Fair question to ask — can I?

Here’s the data:

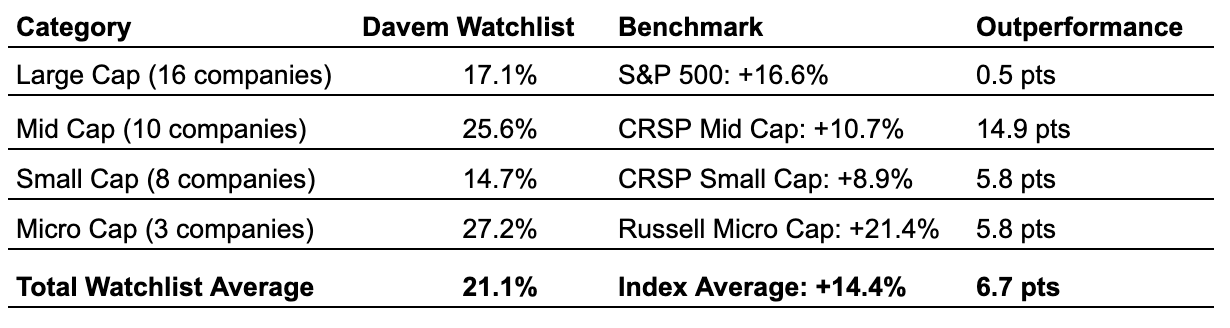

We ended 2025 with 37 companies on the Davem Watchlist. All quality businesses meeting my financial strength criteria. Companies I’d invest in at the right price.

If you created an index and bought equal positions in every watchlist company on January 1, 2025, here’s how you would have done:

The watchlist outperformed in every category.

For context: 65% of professional large-cap fund managers failed to beat the S&P 500 in 2024. Over 15 years, not a single category (large, mid, small-cap, domestic, or international) shows majority outperformance by the professionals.

A focused watchlist of quality companies built with simple criteria anyone can understand beats them all.

But We Don’t Buy the Watchlist

The watchlist identifies what to own. The Davem Method determines when to buy.

The goal isn’t to create another index. It’s to own a few superior companies when conditions warrant. Quality businesses at attractive prices.

So let’s look at actual positions.

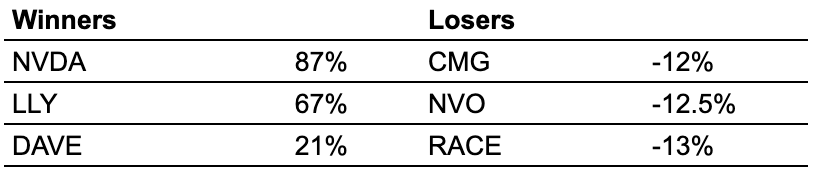

2025 Top Positions:

Average return across all positions: +20.4%

My long-term objective targets a minimum 15% annual return — 5 percentage points above the S&P 500’s 30-year historical average of 10%. The last five years, the S&P averaged closer to 16%, pushing the target to 21%.

I hit the target.

What the Losses Tell You

Notice something about the losers — not more than 13%.

That’s not coincidence, that’s the system.

Early in my investing journey, I took the occasional big loss. The fundamentals remained strong, I had conviction in my thesis. I held on, hoping for a recovery.

But the market doesn’t care about your ideas or conviction.

Those big losses cost me money and confidence. The math to recover is unforgiving. A 50% loss requires a 100% gain just to break even. A 75% loss would take a 300% gain.

So I made a rule that I don’t break: use stop loss orders to never lose big.

Three losing positions this past year all at roughly the same level and no single loss capable of derailing my portfolio gains.

Missed Chances

Each year there are not only wins and losses but also missed opportunities:

$ANET at $85

$FIX at $300

$DECK at $80

I missed these entry points because I hesitated and didn’t trust my own analysis. Different companies, the same “what-ifs” every year.

These behavioral mistakes wouldn’t be solved by paying a financial advisor. They’re only solved by trusting the process every time. That’s not something I can outsource, just work I have to do myself.

I try not to beat myself up over these “what-ifs”, though. I’m in the market long-term and new opportunities always come along. I document the missed chances to learn and because pretending I don’t make mistakes would make me no different than those who only talk about their wins.

The Plan for 2026

The plan for this year? Same as every year.

Identify quality businesses with a track record of financial strength

Wait for attractive prices

Let winners run and cut losses short

I don’t predict where the market is headed. The market will do what it’s going to do.

What I can control is refining my approach and being ready when opportunities present.

Looking forward to what’s ahead in 2026!

What are you excited about this year? Leave a comment and let me know!

Cheers,

Andrew

Coming up in Part III: Is investing too complicated?

Thanks for reading The Davem Dish! If you enjoyed this issue, feel free to subscribe and share it with other awesome people like you.

The content provided are personal opinions and presented for educational purposes only, as of the date published or indicated. Davem Advisors LLC is not a bank, licensed securities dealer, broker or investment advisor. Displayed returns are unaudited. Nothing stated constitutes a recommendation or advice as to whether any investment is suitable for a particular investor. You alone are solely responsible for determining whether any investment, strategy or service is appropriate for your objectives. Past performance is no guarantee of future results. Inherent in any investment is the risk of loss.