Can Anyone Beat the Market?

Investor Deprogramming Series: Part I

Welcome to issue #16 of The Davem Dish. Every two weeks I share what actually works in investing based on my 20 years of wins, losses and expensive lessons. You’ll also get my thoughts on solopreneurship and life in general because the same principles apply — keep it simple, stay consistent and focus on what matters.

Part I of my Investor Deprogramming Series explores whether it’s possible to beat the market. Over the next five posts I’ll dive into “common wisdom” that may be sabotaging your wealth.

Warren Buffett once said “I think I could make a 50% return on $1M”

One of the greatest investors of all time believes “small money” can generate massive returns, yet we’ve been told from a young age that individuals can’t beat the market. The financial services industry continually pushes this narrative citing studies that show it can’t be done because regular people lack expertise, discipline and tools to compete with professionals.

So, the professionals beat the market then, right?

Not exactly. Data from S&P SPIVA shows active management fails at scale. Over the 15-year period ending December 2024, not a single category — large-cap, mid-cap, small-cap, domestic, or international — saw a majority of active managers beat their benchmarks. The longer the time horizon, the worse the results become:

1-year: 65% of large-cap funds underperformed the S&P 500

10-year: Over 80% underperformed

20-year: 94% of domestic equity funds failed to beat their benchmarks

These figures actually understate the problem due to survivorship bias. Over 20 years, nearly 64% of domestic stock funds were liquidated or merged — erasing their poor track records from historical comparisons. The funds that survived represent a positively-selected sample, yet the supposed “cream of the crop” still mostly lost.

How about hedge funds? You know, those exclusive clubs where really smart people make a ton of money.

They fared even worse. From 2009-2019 the average hedge fund returned 6.96% annually versus 13.56% for the S&P 500. A $100,000 investment in 2011 grew to $159,982 by 2020; the same amount in the S&P 500 reached $364,678 — almost 130% more!

You read that right. The smartest people on Wall Street delivered half the returns of doing nothing except buying an index fund.

The Fee Machine

And then there are fees. The math of fees is quite destructive over time. The average actively managed equity fund charges 0.64% in expenses versus just 0.05% for index funds — which may seem insignificant but is a 13x differential.

If you’re “lucky” enough to be able to invest in a hedge fund, the economics are particularly punishing. Under the traditional 2% management fee plus 20% of profits structure, a fund generating 10% gross returns delivers only approximately 6.4% net to you.

Financial advisor fees compound similarly. A 1% annual AUM fee on a $1 million portfolio earning 6% annually will cost you approximately $219,738 over 20 years versus a no-fee alternative — not just from the direct fees, but from the lost compounding on those payments. Combined with underlying fund expenses, a typical advised portfolio faces 1.64% annual drag, reducing your portfolio by 35-40% over three decades.

More about financial advisors in Part II.

Professional Handcuffs

Fees aren’t the only reason why professionals fall short. These are intelligent, experienced money managers but they operate within constraints individual investors don’t face.

SEC rules force mutual funds to spread 75% of assets across multiple positions, with no more than 5% in any single company. This forced diversification prevents managers from concentrating positions in their best opportunities.

Then there’s career risk. Fund managers who take contrarian positions risk losing their jobs if those positions don’t immediately pay off. So, they hug their benchmarks, barely deviating from the index they’re supposed to beat.

Redemption pressure compounds these problems. When markets fall, clients panic and redeem, forcing managers to sell at exactly the wrong time. This creates a vicious cycle: poor performance drives redemptions, which force selling, which creates worse performance.

On the other side, when fund managers do well, money pours in and needs to be allocated, even in overpriced markets creating another drag on performance.

Individual investors face none of these constraints. We can hold a few concentrated positions, don’t have career risk, no short-term reporting, and can enter and exit positions without external pressure forcing our hand.

Why Individual Investors Fail

Despite these advantages, average individual investors underperform benchmarks also but not because of structural constraints but because they sabotage themselves.

Over the 30 years ending 2022, the average individual investor earned 6.8% annually while the S&P 500 returned 9.6% — a gap of 2.8 percentage points per year. This seemingly modest annual difference compounds disastrously. A $100,000 investment over that period grew to approximately $864,000 less for the average investor than for someone who simply bought and held the index.

This gap persists almost every year. In 2024, average individual investors earned 16.5% while the S&P 500 returned 25% — the second-largest gap in a decade at 8.5 percentage points. 2009 was the last year the average investor beat the index. They have now underperformed for 15 consecutive years.

Why do individuals struggle? The primary culprits are excessive trading and behavioral biases.

So, the financial services narrative about how individuals can’t beat the market is true?!

Research from almost 70,000 households found the most active investors earned just 11.4% annually versus 18.5% for passive investors during the same market period. Furthermore, the disposition and endowment effects — selling winners too early while holding losers too long — cost an additional 3-5% annually.

If professionals can’t beat the market because of structural disadvantages and average individuals can’t beat the market because of behavioral mistakes, can anyone beat the market?

Should you just park your money in low-cost index funds and hold for decades?

Well… yes and no.

The Hybrid Strategy

The evidence supports that individual investors who adopt disciplined, low-cost strategies already beat most professionals by default — by avoiding structural disadvantages and behavior traps that plague both groups.

We’re also not average investors. We can stack the odds in our favor with a simple, repeatable process.

Here’s how:

A simple S&P 500 Buy and Hold strategy from January 2009 through 2024 delivered approximately 907% total returns (roughly 15% annualized) — beating 88-94% of actively managed funds over similar periods while requiring zero effort, expertise, or ongoing costs beyond minimal expense ratios.

Buy and Hold doesn’t always work for individual companies as we’ll explore in Part IV.

So, with that, you can use index funds as the foundation for your portfolio and then add a few concentrated individual investments when opportunities appear.

Beat the market by first being in the market, then selectively beating the benchmark.

Using this approach, I’ve booked a +78% profit on $NVDA and am sitting on a +57% unrealized gain in $LLY this year while the S&P 500 is also up +17%.

Of course not all your individual investments will be winners and indexes don’t always rise, but by only investing in quality companies, knowing when to buy and using disciplined selling tools you can let your winners run while minimizing losses.

You don’t need to always be right. You just need to understand patterns and preserve the upside of being mostly right.

This is how you can become better than average, manage your own money and consistently beat the market.

I’ve built my seven-figure portfolio from zero doing this and so can you. The process isn’t complicated, you just need to get started.

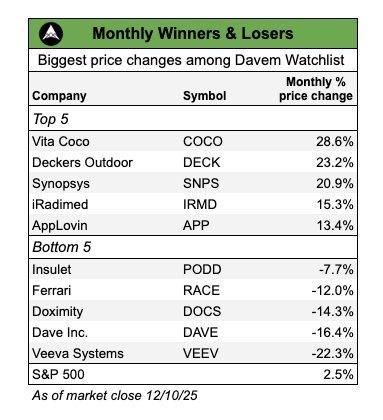

Davem Watchlist Insights

Your edge as an investor isn’t a magic formula, it’s as simple as monitoring your watchlist closely to spot attractive opportunities at the right price.

Let’s first take a look at winners and losers over the last month…

Missed Opportunties:

I have been watching $DECK closely over the past few months. The company has had a rough year on tariff and economic uncertainty fears, but the financial metrics have remained solid — still above my thresholds. Back in early November, I wrote how I saw an opportunity if the stock consolidated ~$80, right at a 3-year support level.

Well, it did exactly that and now shares bounced +23% in a month. My profit? Nothing. I missed out because I hesitated and didn’t trust my own analysis.

Same story earlier this year with $ANET. Stock dropped to a buy level at $85 but again I didn’t pull the trigger. From there, it jumped to a high of $162 and is still up 62% from the $85 buy level.

If your edge is tracking patterns, watching prices closely and being able to spot opportunities, you don’t make money overthinking from the sidelines. I have to occasionally remind myself — use your edge and execute. Not some of the time, but every time.

Challenge:

Drop a ticker in the comments. I’ll show you exactly how I analyze whether a company is a buy or avoid. Free analysis for the first 10 responses. Let’s see if your pick passes my test!

Cheers,

Andrew

Thanks for reading The Davem Dish! If you enjoyed this issue, feel free to subscribe and share it with other awesome people like you.

The content provided are personal opinions and presented for educational purposes only, as of the date published or indicated. Davem Advisors LLC is not a bank, licensed securities dealer, broker or investment advisor. Displayed returns are unaudited. Nothing stated constitutes a recommendation or advice as to whether any investment is suitable for a particular investor. You alone are solely responsible for determining whether any investment, strategy or service is appropriate for your objectives. Past performance is no guarantee of future results. Inherent in any investment is the risk of loss.