Data Centers Aren’t Draining America

Welcome to issue #31 of The Davem Dish. Every week I share what actually works in investing based on my 20 years of wins, losses and expensive lessons. You’ll also get my thoughts on solopreneurship and life in general because the same principles apply — keep it simple, stay consistent and focus on what matters.

Every few weeks a new headline claims data centers are draining lakes, hollowing out aquifers, or sucking small towns dry to feed the AI boom.

A hyperscale facility uses 5 million gallons a day. ChatGPT burns through a bottle of water every hundred words. Phoenix is parched and the tech giants keep building anyway.

Some of those claims are accurate in narrow ways. Most are misleading once you back them out. The more interesting story, with actual investing implications, sits underneath it all.

This post has two halves. The first walks through the receipts on data center water use — what’s true, what’s exaggerated, and where the real industrial shift is happening. The second is the part where investor money is actually won or lost. Spotting a trend in the world doesn’t tell you what to buy. The work is finding a business that deserves to be owned in that trend at a price that makes sense.

The Numbers Most People Don’t See

Let’s start with the headline water figure. U.S. data centers directly consumed about 17.4 billion gallons of water in 2023, or roughly 48 million gallons per day. Total U.S. water withdrawal sits at around 322 billion gallons per day. Data centers represent less than 0.02% of the national total. Even adjusting for the fact that most withdrawn water gets returned to the watershed, the share stays well under 0.1% — a rounding error compared to agricultural irrigation, which accounts for roughly 42% of U.S. withdrawals and the majority of consumptive use.

Even the dramatic sounding “5 million gallons a day at one site” figure deserves context. That’s an upper-bound number for a large hyperscale facility on a hot day, not an average. Google’s reported data is the cleanest public dataset we have, and most of their 24 U.S. and Canadian sites use a fraction of that. Their largest site in Council Bluffs, Iowa consumed about 2.8 million gallons a day in 2024. Most of the rest are well below 1 million.

The nuance is in the gap between water withdrawn and water consumed, and most reporting doesn’t separate them. When a data center withdraws water, some fraction returns to the local watershed as discharge. The rest evaporates out of cooling towers and is gone — for that particular watershed — until it falls again as rain somewhere else. For evaporative-cooled facilities, 70 to 80% of withdrawn water typically evaporates. So the headline “they’re using a billion gallons” is technically accurate but doesn’t separate the gallons returned from the gallons that are actually gone.

The Full Picture

Data centers themselves are a small share of national water consumption. The picture changes when you add up everything the AI buildout actually requires.

Thermoelectric power plants — coal, natural gas, nuclear — withdrew 52.8 trillion gallons in 2017, the last comprehensive federal figure. They account for around 40% of total U.S. water withdrawals. Coal plants use roughly 19,000 gallons of water per megawatt-hour. Natural gas plants use closer to 2,800. Most of that water is returned, but the actual consumption number for the U.S. fleet still runs to about 3 billion gallons per day. Every kilowatt-hour a data center uses carries a water footprint upstream at the power plant.

Semiconductor fabrication facilities (fabs) are the thirstier piece of the chain on a per-site basis. An average chip fab uses around 10 million gallons of ultrapure water per day, comparable to roughly 33,000 households. Taiwan Semiconductor’s Arizona fab will draw 8.9 million gallons a day to operate one site. Intel’s Ocotillo campus, also in Arizona, is modeled at 14 million gallons a day across three advanced fabs.

So the AI water footprint has three layers stacked on top of each other. The data center itself withdraws water for cooling. The power plant that feeds it withdraws water for thermoelectric generation. And the fab that builds its chips withdraws water for wafer processing. Stack them together and the total is larger than any single facility suggests, but it also makes the picture more complicated, because those three layers don’t sit in the same place geographically.

Geography Matters

The reason any of this becomes controversial is concentration. Data centers cluster. About 40% of U.S. data centers sit in regions classified as high or extreme water stress. Phoenix hosts more than 58 facilities. Loudoun County, Virginia is the densest data center market in the world. Together those two regions account for a meaningful share of the national footprint.

A 0.02% national water share doesn’t mean much when dozens of facilities are pulling from the same desert aquifer. Local capacity is what matters, not the country-wide average. Phoenix’s water utility doesn’t care that Michigan has water to spare. So while the national alarmism is overstated, the regional pressure is real, and it’s pushing operators to change how they cool facilities.

Which raises the obvious question — why build in Arizona at all? Because everything else about the location works. Dry desert air is ideal for cooling and chip manufacturing because low humidity prevents corrosion and condensation on sensitive equipment, and evaporative cooling works more efficiently in dry conditions than in humid ones. The state offers cheap, flat, developable land at a scale that doesn’t exist on the coasts. It has minimal earthquake, hurricane, and tornado risk. It has mature power infrastructure including the country’s largest nuclear plant and significant solar generation. It has aggressive tax incentives, expedited permitting, an educated workforce and a dwindling but managed water supply backed by Colorado River allocations and groundwater reserves. Roughly 70% of state water currently goes to low-value agriculture like alfalfa and cotton, where a million gallons used by a semiconductor fab supports orders of magnitude more high paying jobs than the same water in alfalfa. Reallocation from agriculture to industry is a policy lever the state has, and is using.

The neighbors have their own constraints. Nevada has weaker Colorado River rights and less groundwater. New Mexico is smaller, less regulated, and just lost a Supreme Court case forcing it to cut pumping. Texas has its own electric grid problems. Each southwest location has its tradeoffs, and Arizona’s happen to favor industrial use.

What the Operators Are Doing

Three shifts are already underway.

The first is a slow move away from open-loop evaporative cooling toward closed-loop systems. Closed-loop cooling can reduce water consumption by 70 to 90%, at the cost of higher electricity use. Microsoft’s newest data center designs are targeting near-zero evaporative loss, with pilot facilities expected this year. Google’s air-cooled site in Pflugerville, Texas used about 270 times less water per day than their evaporative-cooled Iowa site in 2024. The design choice was the difference.

The second is a change in the input source. Reclaimed wastewater, treated industrial water, and other non-potable supply are replacing drinking water at a growing number of facilities. Google reported reclaimed water accounted for about 22% of their cooling volume in 2023. Across the broader industry it remains under 5%.

The third is direct-to-chip and immersion cooling, where the coolant goes straight to the server hardware rather than through cooling towers at all. These approaches use less total energy and far less water but require purpose-built infrastructure and different facility designs.

All of this is in motion. Companies build whole product lines around it. Which is where the investing question finally enters.

Spotting the Trend Is the Easy Part

This is where a typical investing newsletter would list five stocks “set to benefit from the data center water shift” and expect you to follow along and buy or name a relevant ETF that holds a basket of these companies.

That isn’t how my process works.

Identifying the direction of an industry is relatively straightforward. Finding a specific business that participates in that shift and deserves to be owned is a separate question. Most thematic stocks fail their fundamentals test. Some are unprofitable, and others are diversified industrial companies where the relevant business unit is too small to move the share price. A few have the right exposure but the wrong valuation. And an ETF basket mixes a couple good companies with several not so good companies.

So let’s begin with the candidate universe. Two categories are worth evaluating — cooling and thermal management for the data center itself, and water treatment and recycling for the input side. None of these are recommendations.

Cooling and thermal management

Vertiv Holdings, Modine Manufacturing, AAON, Munters, Trane Technologies, Johnson Controls, and Carrier Global.

Water treatment and recycling

Xylem, Pentair, Watts Water, A.O. Smith, and Ecolab.

The next step is running each through our process. That means putting them through the same screen as any other company: financial quality of the business, valuation, operating history, margin trajectory, and capital allocation.

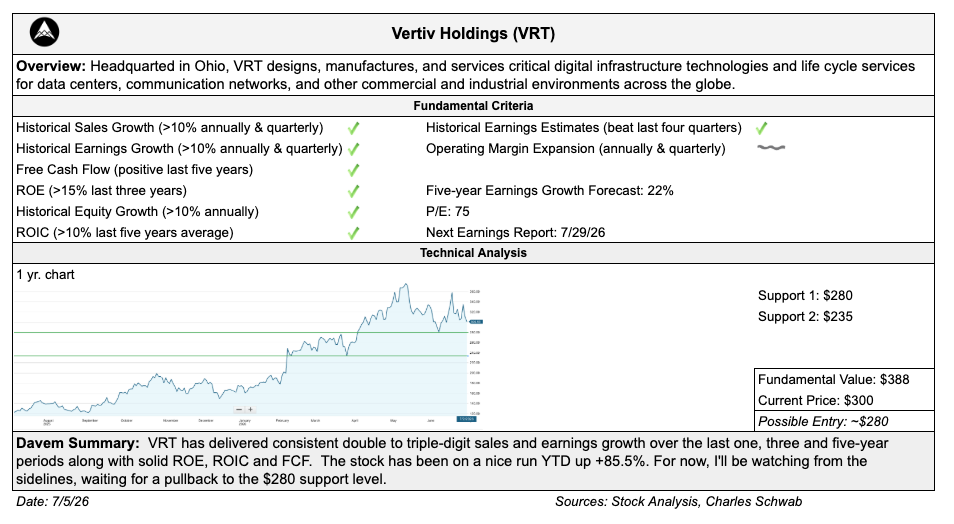

Of the twelve names on the list, only Vertiv Holdings (VRT) passed the screen. Here’s what that looks like:

Vertiv checks the boxes the Davem Method requires — consistent double and triple-digit sales and earnings growth over one, three, and five-year windows, solid returns on equity and invested capital, healthy free cash flow, and a forward growth forecast that supports the story going forward. Fundamental value works out to $388 against a current price near $300, which puts the stock in undervalued territory.

But I’m still not buying it here.

The stock has run 85% year to date, and support at $280 gives a cleaner entry with a better margin of safety. Waiting for that level costs me nothing if it comes. Chasing a name because the underlying trend is compelling is how investors turn good analysis into bad returns. Vertiv earns a spot on the watchlist for now. If price meets fundamentals, it becomes a buying opportunity. Until then, I sit back and watch.

That’s the ending. Not a buy or a pass. A name that’s earned the right to be waited on.

Most investors won’t do this. They want the trend to do the work — a shift in the world to hand them a return. The trend can’t do that. It only tells you where to look. The fundamentals tell you whether to buy, and the price tells you when.

Simple but not easy.

This is the summary version of how I evaluate an idea. Stock Selection Simplified is the full walkthrough. Every screen, valuation step, and judgment call, laid out in the order I use them. If you want to run this same process on your own ideas, the guide is where the details live. Founding Rate is good until August 1st.

Thanks for reading The Davem Dish! If you enjoyed this issue, feel free to subscribe and share it with other awesome people like you.

The content provided are personal opinions and presented for educational purposes only, as of the date published or indicated. Davem Advisors LLC is not a bank, licensed securities dealer, broker or investment advisor. Displayed returns are unaudited. Nothing stated constitutes a recommendation or advice as to whether any investment is suitable for a particular investor. You alone are solely responsible for determining whether any investment, strategy or service is appropriate for your objectives. Past performance is no guarantee of future results. Inherent in any investment is the risk of loss.